The Fixed Deposit Trap: Why Your “Safe” Retirement Plan May Be Failing You

Fixed Deposits feel safe, but over long retirement horizons, they often fail to keep up with inflation. Discover how rising costs quietly erode FD returns and why disciplined mutual fund investing offers a smarter path to preserving purchasing power and building long-term wealth.

Kartikay Ungrish

1/11/20268 min read

The Comforting Illusion of Safety

Fixed deposits have long occupied a central place in the minds of investors seeking stability, predictability, and peace of mind. For decades, they've been promoted as the safest and most dependable way to park money—especially for people nearing retirement or depending on their savings to generate regular income.

The idea is simple and reassuring: you invest a lump sum, the bank promises a fixed rate of return, and you receive interest at regular intervals. No market swings to worry about. No complex products to understand. No daily monitoring required.

This simplicity has made fixed deposits the default choice for conservative investors and retirees alike. But what if this "safety" is actually putting your retirement at risk?

However, as comforting as this approach feels, the illusion can be financially fatal in the long term, and it deserves a closer, more critical examination, particularly when the goal is to generate income over a long period, such as twenty or thirty years. Retirement today is no longer a short phase at the end of life. Advances in healthcare, improved living standards, and better awareness mean that people are living longer than ever before. Many individuals now spend as much time in retirement as they once spent building their careers. In such a scenario, the question is not just whether your money is safe, but whether it is working hard enough to support you throughout this extended phase of life.

The Silent Killer: Inflation Is Eating Your Savings Alive

The real risk in retirement planning is not market volatility alone. It's the slow and often invisible erosion of purchasing power caused by inflation.

Inflation steadily increases the cost of living year after year. What feels like a comfortable income today may become inadequate—even insufficient—a decade later. Your ₹3 lakh annual income might cover your expenses comfortably now, but will it be enough in 2040?

Fixed deposits, while nominally safe, often fail to address this challenge. When returns barely exceed inflation—or worse, fall below it—the investor experiences what can be called silent wealth destruction. The capital may appear intact on paper, but its real value steadily declines.

You're not preserving wealth. You're watching it disappear in slow motion.

To understand this more clearly, consider how fixed deposits actually work in practice. When you place money in a fixed deposit, you agree to lock in your funds for a specific period, ranging from a few months to several years. In return, the bank offers a fixed interest rate. This rate does not change during the tenure of the deposit, regardless of what happens in the broader economy. Interest may be paid monthly, quarterly, or annually, or compounded and paid at maturity.

This structure provides predictability. You know exactly how much income you will receive and when. For example, an investor who places 50 lakh rupees in a fixed deposit earning 6% annually can generate roughly 3 lakh rupees in interest per year. Over thirty years, this amounts to total withdrawals of ninety lakh rupees. At the end of this period, the original capital of fifty lakh rupees still remains. On the surface, this appears to be an excellent outcome. The investor has enjoyed steady income without touching the principal.

But this is where the illusion begins. The three lakh rupees received in the first year does not have the same value as the three lakh rupees received in the twentieth or thirtieth year. Over time, inflation raises the cost of essentials such as food, housing, utilities, healthcare, and transportation. Medical expenses, in particular, tend to rise faster than general inflation, and they often become a significant part of a retiree's budget.

Negative Real Returns: You're Losing Money While Thinking You're Safe

If inflation averages 5% to 6% over long periods, a fixed deposit earning 6% offers little to no real growth. In some years, inflation may even exceed the interest rate, resulting in negative real returns.

This means that although the investor continues to receive the same nominal income, their ability to maintain their lifestyle gradually diminishes. You might still get your ₹3 lakh every year, but it buys less and less.

The fixed deposit feels safe, but it does not protect against the most important risk in retirement: the risk of outliving your money or seeing its purchasing power shrink to uncomfortable levels. You're not being cautious—you're being reckless.

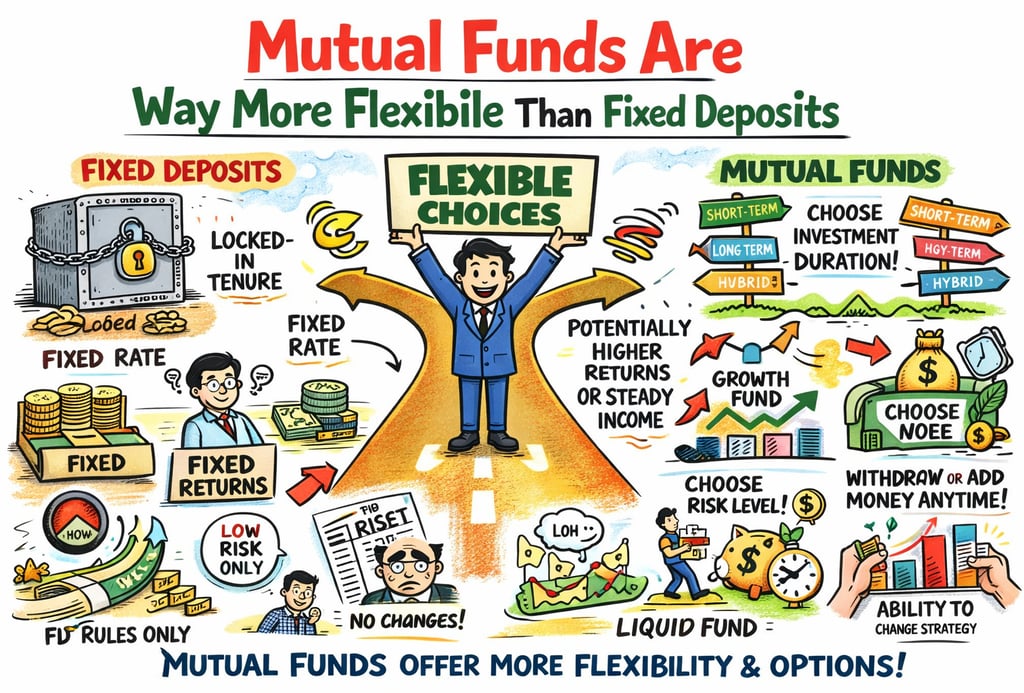

Trapped in Your Own Investment: The Flexibility Problem

Another limitation of fixed deposits is their lack of flexibility. While they're easy to understand, they often come with penalties for premature withdrawal.

Life, especially in retirement, can be unpredictable. Medical emergencies, family needs, or unexpected expenses may require access to capital. Breaking a fixed deposit early can result in reduced interest or penalties, further lowering already modest returns.

When you need your money most, your "safe" investment locks you out.

This brings us to a broader and more important question. Is safety alone enough when planning for long-term income, or should safety be redefined to include protection against inflation and longevity risk? True financial safety in retirement is not just about preserving capital in nominal terms. It is about ensuring that income remains adequate throughout life, regardless of how long one lives or how prices change.

This is where alternative income strategies, such as systematic withdrawal plans from growth-oriented investments, come into the picture. A systematic withdrawal plan, often implemented through mutual funds, allows an investor to withdraw a fixed amount or a percentage of their investment at regular intervals. Unlike fixed deposits, these investments are typically linked to assets such as equities, which have higher long term growth potential.

Many investors hesitate at this point because equities are inherently volatile. Prices go up and down, and short-term losses are possible. However, over the long term, equities have historically delivered returns that comfortably exceed inflation. This excess return, often referred to as real return, is what makes them powerful tools for long-term wealth creation and income generation.

Consider the same fifty lakh rupees invested in a diversified equity-oriented mutual fund portfolio. Assume a long-term average return of twelve percent, which is a reasonable assumption based on historical data over extended periods. Now imagine withdrawing 6% of the initial investment each year, which again amounts to 3 lakh rupees annually. Over thirty years, the total withdrawals are the same as in the fixed deposit example: 90 lakh rupees.

The crucial difference lies in what happens to the remaining corpus. Since the investment grows faster than the withdrawal rate, the capital continues to compound. Despite regular withdrawals, the portfolio does not merely survive; it grows. At the end of thirty years, the remaining corpus can be close to three crore rupees, many times the original investment. This growth is not the result of speculation or market timing. It results from allowing compounding to work over long periods while maintaining a disciplined withdrawal strategy.

This outcome changes the entire retirement equation. Instead of worrying about whether your capital will last, you now have a growing cushion that can absorb inflation, unexpected expenses, and longer lifespans. The income stream remains sustainable, and the investor retains flexibility. Withdrawals can be adjusted if needed, and the remaining corpus continues to work in the background.

You Don't Have to Abandon Safety—Just Redefine It

It's important to emphasize that this approach does not mean abandoning safety altogether. A well-designed systematic withdrawal strategy does not rely solely on equities.

Asset allocation plays a critical role. By combining equities with debt instruments and rebalancing periodically, investors can manage volatility while still benefiting from long-term growth.

The goal is not to chase high returns, but to ensure the portfolio's growth rate exceeds the withdrawal rate. Smart risk, not reckless risk.

Structure Matters More Than You Think

One of the most common mistakes investors make is focusing only on returns without considering the structure of income. In retirement, the sequence of returns and withdrawals matters.

A thoughtful withdrawal plan accounts for market cycles, adjusts withdrawals when necessary, and maintains adequate liquidity for short-term needs. This level of planning is absent in traditional fixed deposit-based strategies, which assume that stability alone is sufficient.

It's not. And assuming otherwise could cost you dearly.

Another aspect worth considering is taxation. Interest income from fixed deposits is typically taxed at the investor's applicable income tax rate. This further reduces the effective return, especially for individuals in higher tax brackets. In contrast, withdrawals from mutual funds may be taxed more efficiently, depending on the investment's nature and holding period. Over the long term, this difference in taxation can significantly affect net income and wealth accumulation.

Don't Let Fear Make You Poor

Behavioral comfort is often cited as a reason for sticking with fixed deposits. Investors feel uneasy seeing market values fluctuate, even if they don't intend to sell.

This emotional response is understandable, but it can be managed through education and proper planning. When the focus shifts from short-term market movements to long-term income sustainability, volatility becomes easier to tolerate.

Regular withdrawals can continue even during market downturns, provided the overall strategy is sound and diversified. The real danger isn't volatility—it's letting fear lock you into a losing strategy.

Fixed Deposits Aren't Evil—They're Just Misused

It's also worth noting that fixed deposits play a role in retirement planning. They're not inherently bad or useless.

For short-term needs, emergency funds, or individuals who cannot tolerate any volatility, fixed deposits provide certainty and peace of mind. The problem arises when they're used as the sole or primary source of income for long-term retirement needs.

In such cases, their limitations become increasingly evident over time. Use them wisely, not exclusively.

A balanced retirement strategy recognizes that different goals require different tools. Short-term expenses and near-term withdrawals can be funded through safe instruments such as fixed deposits or short-term debt funds. Long-term income needs, on the other hand, require growth-oriented assets that can beat inflation. By combining these elements, investors can create a more resilient and adaptable income plan.

Longevity risk is another factor that deserves serious attention. No one knows how long they will live, but there is a real possibility of living well into one's eighties or nineties. Planning for a shorter lifespan can lead to underestimating future expenses and overestimating the adequacy of fixed income sources. A growing corpus provides a margin of safety against this uncertainty. It allows retirees to maintain their standard of living without constantly worrying about running out of money.

Healthcare Costs Will Skyrocket—Is Your Income Ready?

Healthcare costs, which tend to rise sharply with age, further complicate the picture. Fixed-income streams that don't grow in real terms may struggle to cover these expenses.

Growth-oriented withdrawal strategies, by contrast, offer a better chance of keeping up with rising costs. They also provide flexibility to increase withdrawals if needed, without immediately depleting the entire corpus.

When a medical emergency strikes at 80, you can't go back and fix your investment strategy.

The Bottom Line: Safety Is Not Enough

The traditional view of fixed deposits as the ultimate solution for retirement income needs to be reexamined. While they offer nominal safety and predictability, they fall short when evaluated against the realities of inflation, longevity, taxation, and rising expenses.

True financial security in retirement comes not from avoiding all risk, but from managing risk intelligently. Playing it "safe" with fixed deposits might be the riskiest move you make.

The Smarter Path Forward

A disciplined, systematic withdrawal approach, supported by appropriate asset allocation and regular review, offers a more robust solution for long-term income.

It delivers the same regular cash flow that investors seek, while also preserving and growing capital over time. This combination of income and growth is what allows retirees to face the future with confidence rather than anxiety.

You can have stability and growth. You just need to stop settling for outdated strategies.

Ultimately, the choice of income strategy should align with the investor's time horizon, risk tolerance, and financial goals. For short-term needs and extreme risk aversion, fixed deposits may be appropriate. For long-term retirement planning, however, an approach that balances growth and stability is far more likely to deliver lasting financial independence. The real measure of safety is not whether your capital remains unchanged on paper, but whether it continues to support the life you want to live, year after year, without compromise.

With the right guidance, you don't have to constantly track markets, rebalance portfolios, or fear emotional decisions during volatile times. A trusted advisor brings clarity, discipline, and peace of mind—helping your investments stay on course while you focus on what truly matters. At Worthy Capitals, we specialize in building and managing mutual fund portfolios with long-term wealth creation at the core. Take the first step today by sharing a few basic details, and let us do the heavy lifting.

Invest & Insure Wisely!

Secure your financial future with us.

Call us / WhatsAPP us / Email Us Your Query

Or drop your Email ID, We will contact you!

help@worthycapitals.com

08586875150

© 2025. All rights reserved.