What is a Specialized Investment Fund (SIF)?

A Specialized Investment Fund (SIF), a SEBI-regulated, exclusive pooled investment vehicle, is designed to offer investors institutional-grade investment strategies that are not available to traditional mutual funds. It maintains significantly lower minimum entry requirements (Rs. 10 lakhs) than PMS (Rs. 50 lakhs) or AIFs (Rs. 1 Crore), making it accessible to a broader range of investors. This lower minimum investment ensures SIFs serve a wider audience, including those with smaller investment amounts.

SIFs, with their unique combination of diversification, liquidity, and tax efficiency similar to that of mutual funds, along with the active strategy and alpha generation capabilities found in high-ticket products, hold the promise of delivering better risk-adjusted returns. They achieve this by using tactical allocation, a strategy that adjusts the portfolio's asset allocation based on short-term market conditions, derivatives, and advanced portfolio construction techniques. This approach allocates 25 percent of total capital to unhedged short positions in equities to capitalize on declines as opportunities arise.

These benefits make SIFs particularly suited for mass-affluent investors (₹10–50 lakh) who seek more sophisticated, actively managed portfolios but cannot (or prefer not to) cross the ₹50 lakh PMS or ₹1 crore AIF thresholds. With SIFs, investors can invest with confidence, knowing they have access to institutional-grade strategies that are well-regulated and offer the potential for better returns, instilling optimism and hope for their financial future.

How is SIF different from other regulated investment products?

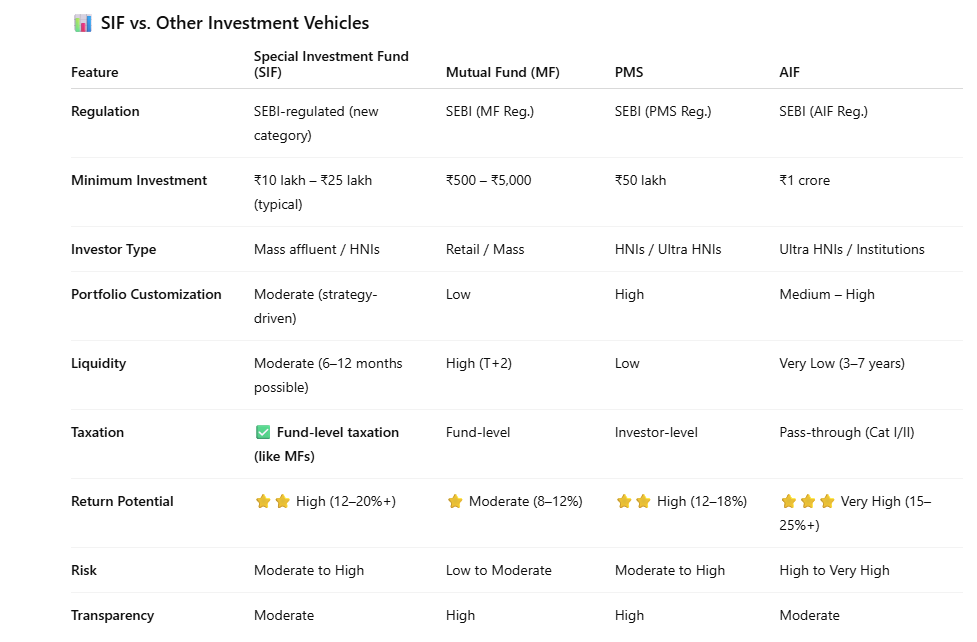

The Specialized Investment Fund (SIF) offers you a unique opportunity to bridge the gap between traditional mutual funds and advanced, regulated products, such as Portfolio Management Services (PMS) and Alternative Investment Funds (AIF).

PMS are professional services offered by portfolio managers who manage your investments on your behalf. At the same time, AIFs are highly customised funds that invest in assets such as stocks, bonds, and real estate. Both come with high entry barriers of Rs 50 Lakhs and Rs 1 Crore, respectively, and are thus limited to HNIs and Ultra HNIs.

SIF Taxation in India

Investing in Specialized Investment Funds (SIFs) offers significant tax advantages. Unlike traditional PMS (Portfolio Management Services) and AIF (Alternative Investment Fund) structures, SIFs have a straightforward tax structure. They are taxed at the fund level, meaning the fund itself handles income tax payments—just like mutual funds. This simplicity not only reduces complexity but also positions SIFs as an appealing option for high-ticket investors seeking ease of management.

To put it simply, here are the compelling benefits of SIFs:

- Investors won't face taxation on individual portfolio transactions or trading activities, allowing you to focus on your investment strategy.

- Capital gains tax applies only when you redeem your investment, and it varies based on the underlying asset class and holding period.

This tax-efficient framework gives SIFs an edge over PMS and AIF, providing investors with substantial financial benefits and enhancing confidence in their investment decisions. The tax savings from SIFs can compound over time, leading to better overall returns for the investors and providing reassurance about their investment strategy.

By choosing SIF, even a middle-income investor can access sophisticated investment strategies that drive better returns and foster wealth creation. The chart below outlines the key differences and similarities between SIF and other popular investment avenues, including mutual funds, PMS, and AIF. Have a glance:

Understanding the Potential of SIF Strategies

1) Equity Long-Short Fund

Purpose: Capture alpha by going long undervalued stocks and shorting overvalued ones — generating returns independent of market direction while managing downside. SEBI requires an equity allocation of around 80%.

Typical benchmark: AMCs often use a broad equity total-return index (e.g., NIFTY 50 TRI or NIFTY 500 TRI) or a custom “long-short” peer benchmark — but check the ISID for the fund’s official benchmark.

Risk profile (benchmark vs fund):

Benchmark risk: A broad equity TRI has market/systematic risk (beta), concentration risk, and is sensitive to macro cycles.

Fund risk: higher implementation risks — model/stock-selection risk, short squeezes, counterparty/derivatives execution risk, leverage/rollover costs, and tracking/manager risk. The fund may have a lower correlation with the benchmark but can still experience significant drawdowns if short positions or hedges fail. SEBI caps naked unhedged short derivative exposure (typically 25% NAV) to limit tail risk.

Track record: AMCs (DSP, Quant) publish simulated backtests showing historical alpha, but past simulated performance ≠ future returns; slippage and costs matter.

Philosophy: Stock-picker’s alpha + risk management — profit from relative mispricings while limiting net market exposure. Works best when dispersion across stocks is high, and the manager’s forensic research (or quant signals) identifies persistent edges.

2) Equity Ex-Top-100 Long-Short Fund

Purpose: Same long-short approach but constrained to stocks outside the top-100 by market cap (i.e., mid & small caps). Designed to exploit inefficiencies in less-covered companies. SEBI mandates a minimum allocation (e.g., ~65%) to ex-top-100 names.

Benchmark: NIFTY MidSmall, NIFTY 500 TRI, or custom ex-top-100 index (check ISID).

Risks: Benchmark has higher volatility, idiosyncratic, and liquidity risk. Fund adds greater dispersion (boosts alpha but increases volatility), higher execution costs, and larger drawdowns when mid- and small caps de-rate. Small-cap shorting raises execution risk.

Back-tested returns: Quant/AMP teams (e.g., Quant Mutual Fund’s QSIF filings) have published simulated performance or model portfolio returns for ex-top-100 strategies in filings/presentations; however, live track records are limited because these SIFs are new. Example: quant filed schemes and published NFO/ISID materials describing objectives and simulated projections. Check the specific QSIF ISID for any model returns.

Why it works: Thin analyst coverage creates mispricings. Exploit information edge in SMID stocks while hedging market exposure.

3) Sector-Rotation Long-Short Fund

Purpose: Concentrated bets across up to 4 sectors — long outperformers, short underperformers — to harvest cyclicality and rotation.

Typical benchmark: A broad equity index (e.g., NIFTY 50 TRI or sector-weighted custom benchmark) or a composiBenchmark: NIFTY 50 TRI or sector-weighted custom composite (see ISID). Higher coRisks: Benchmark has sector concentration. Fund adds high sector concentration, macro/cycle correlation, positioning risk on sharp moves, and short squeeze/liquidity issues. SIF ISIDs typically describe strategy and historical scenarios rather than long-run live returns. Expect AMCs to present multi-period simulated scenarios rather than long-lived track records (new product).

Why it works: Exploit macro, earnings, and capital-cycle differences between sectors with high-conviction, hedged bets.

4) Debt Long-Short Fund

Purpose: Apply long-short logic to the debt market — take long positions in bonds/credit expected to perform and use exchange-traded debt derivatives or futures to short interest-rate/credit exposures. Aim: generate alpha from rate/credit view and manage duration & spread risk more actively than typical debt funds.

Benchmark: CRISIL Composite, G-Sec index, or custom duration/credit composite (see ISID).

Risk profile:

Benchmark risk: interest-rate risk, credit risk, and liquidity of the underlying bonds.

Fund risk: Execution/derivative basis risk, counterparty risk on derivatives, complexity of hedging strategies, and credit event risk (default). Shorting in debt markets involves basis and collateral costs.

Back-tested returns: Limited public backtests from AMCs for debt long-short SIFs exist publicly — some institutional teams present model returns for active fixed-income strategies, but these are typically scenario-based and sensitive to assumptions about roll/yield curve changes. Example: ISID and AMC presentations describe strategy risk/return tradeoffs.

Why it works: Express rate and credit views while hedging uncompensated duration/credit risk.

5) Sectoral (Debt) Long-Short Fund

(Sometimes referenced as “Sectoral Long-Short Fund” for debt)

Purpose: Focus debt exposure on one or more sectors’ issuers (e.g., banking, infrastructure) and use long/short or hedging in debt instruments of those sectors to exploit relative credit moves. SEBI permits sectoral debt SIFs with limits (e.g., a maximum % in a single sector).

Benchmark: Sectoral credit index or custom composite (see ISID).

Risks: Benchmark has sector concentration and issuer risk. Fund adds high single-sector concentration, default and liquidity risk, plus correlation spikes in stress.

Track record: Few live returns (new product) — AMCs show hypothetical scenarios and credit-cycle models.

Philosophy: Deep sectoral credit research — exploit relative value between issuers in a sector and hedge macro/interest risk via derivatives.

6) Active Asset Allocator Long-Short Fund (or Active Asset Allocator)

Purpose: A multi-asset, dynamic allocator that can shift between equities, debt, REITs/InvITs, commodities, and use long/short exposures across these asset classes to seek returns and manage downside. Intended for investors who want a single strategy that actively times/risk-allocates across asset classes.

Typical benchmark: Composite multi-asset benchmark (e.g., blended index based on target allocations — AMCs define it in ISID). There’s no single market benchmark; AMCs usually provide a peer composite.

Risk profile:

Benchmark: Risk of multi-asset benchmarks depends on underlying allocations and can be moderate with a balanced allocation.

Fund: Strategy risk comes from allocation/timing decisions, model/quant errors across asset classes, and cross-asset derivative risks. Liquidity differences across assets create execution risk.

Back-tested returns: Some AMCs (e.g., SBI/Altiva/Edelweiss presentations) have sample backtests showing how dynamic allocation would have performed across past cycles; these are usually illustrative and vary materially with assumptions. Example: SBI Magnum and Edelweiss Altiva materials describe hybrid/asset-allocator SIF products.

Philosophy: Diversify sources of returns — combine tactical asset allocation with long/short overlays to reduce drawdowns and capture cross-asset opportunities.

7) Hybrid Long-Short Fund (Hybrid)

Purpose: Consistent equity-debt blend (SEBI minimum ~25% each) with limited short exposure via derivatives for hedging and alpha — hybrid exposure with active risk management.

Benchmark: Blended equity+debt (e.g., 60:40 or custom) per ISID.

Risks: Benchmark has blended market risk. Fund adds complexity in managing two asset classes (rebalancing, correlation shifts), hedge implementation risk, and combined equity-debt exposure.

Back-tested returns: AMCs launching hybrid SIFs (e.g., SBI’s Magnum Hybrid Long-Short Fund, Quant’s hybrid filings) publish product decks and sometimes simulated performance. Those show how a hybrid long-short overlay might have reduced drawdowns compared with pure long-only hybrid portfolios—again, largely model- and simulation-based.

Why it works: Hedged positions across assets deliver smoother returns than equity long-short and better upside than conservative hybrids.

Important practical notes & caveats

SEBI rules and ISID disclosures govern minimums, caps (e.g., max unhedged short = 25% NAV), redemption frequency, and instruments — check each fund’s ISID.

AMCs choose benchmarks (index or custom) — confirm in ISID.

AMC backtests (DSP, Quant, SBI, Edelweiss) are mostly simulated—useful but sensitive to costs, slippage, survivorship bias, and overfitting. Treat cautiously.

SIFs are new (2025–2026) — live track records are still building. For specific fund performance, provide the fund name for the latest NAV/history.

Ideal Investor Profile for SIFs

SIFs are tailored for investors who seek higher returns and tactical alpha beyond traditional mutual funds. They appeal to those wanting:

- Institutional-style strategies that offer tax efficiency and lower barriers compared to PMS/AIF.

- Moderate liquidity (6–12 months) and are comfortable navigating slightly higher complexity.

- Focused volatility management and drawdown control through innovative long-short strategies.

Now that you’ve understood the power of Specialized Investment Funds (SIFs) and how they unlock an exciting wealth-creation opportunity for mid- to upper-level retail investors, it’s time to take the next step with confidence. You can invest in all SIFs seamlessly through Worthy Capitals — a trusted financial services and mutual fund distribution firm, operated by an NISM- and AMFI-registered distributor (ARN 276810). What sets us apart is our expertise: Kartikay, founder of Worthy Capitals, is among the first few mutual fund distributors in India to clear the highly competitive NISM-Series-XIII: Common Derivatives Certification, a mandatory qualification for advising and distributing SIFs. His early adoption of this certification will reassure you that you are investing with a pioneer, ensuring that your investments are guided by deep knowledge, regulatory compliance, and a commitment to maximizing your wealth potential. Take full advantage of Worthy Capitals’ expertise today and let your SIF journey begin with confidence.

Invest & Insure Wisely!

Secure your financial future with us.

Call us / WhatsAPP us / Email Us Your Query

Or drop your Email ID, We will contact you!

help@worthycapitals.com

08586875150

© 2025. All rights reserved.